January Spending Report

Putting Our Cards on the Table

In an effort to keep myself accountable to the idea that doctors do not have to spend a totally ridiculous amount of money to live well and love life, I’ve decided to share our spending for last month (and hopefully all months in 2018, assuming I can stay that organized).

Notice that we call it “spending” and not “expenses” or “costs of living” or anything else that implies that our use of our money is something that just happens to us while we sit there in helplessness.

As I may have mentioned before, we do not do traditional budgeting. You absolutely should do traditional budgeting if that works for you as a way to control your spending. More on this topic here.

Notes About These Numbers

-I have not included our charitable giving here, which can be a very sensitive subject for a lot of people (especially those who feel like they are drowning in debt). But unless you yourself are about to starve or freeze to death due to lack of basic resources, I recommend you find at least one charitable organization you are really excited about and send them monthly donations via auto-draft, even if it’s a small amount. Many charities desperately need people who can commit to monthly financial support.

-This list does not include our HSA, stock investments, or our real estate investments. I am planning to write more about how we approach our savings and investments soon.

-This list does not include business loan payments, professional dues, licensing fees, malpractice insurance, or other expenses that are due exclusively to our business ownership and – unlike my student loans – would go away if I sold the business and switched careers.

-The student loan payment shown is what I have on auto-draft. You can read here about how we are paying extra on our loans every month in an effort to be done with them this year. I include student loans in “home” spending even though they are related to my career because they don’t go away no matter what I do career-wise.

-We have health insurance and an HSA though my husband’s work as a teacher, both of which are deducted directly from his paycheck. It’s actually a pretty great deal, all things considered. We pay out of pocket for dental care and eye care services as needed.

-All “Entertainment/Dining” expenses are 100% optional expenses. For us, these tend to be things like going to the movies and eating at Chick-fil-A.

-I include life and disability insurance in this list even though they are sort of related to work, because they are what protect our current lifestyle. My disability insurance is expensive because it is important to us to be able to pay off all our debts and live well even if I am unable to work.

-“Groceries” includes food, household items, medications, and toiletries purchased at Sam’s Club or grocery stores or Walgreens.

-I have separated baby formula out because it is a significant expense that will not apply to everyone and will go away in a few months for us. All other baby-related expenses are included in “Grocery/Pharmacy”. You can read about how we got all ready for our baby for less than $350 here.

-Utilities are rarely any higher than this since it’s winter and we were home for most of the month.

-This list does not include at-home babysitters, who we occasionally pay in cash to watch our kids. Any at-home babysitters we pay are non-essential, although very much appreciated. The daycare we pay for while we are both at work (which is very much essential as long as we both want to work) is listed under “Daycare”.

-The category called “$ Earned by Little C” is what our 11 year-old earns by doing things like reading out loud for the family and doing miles on the treadmill ($0.20 per mile). We don’t do a traditional allowance.

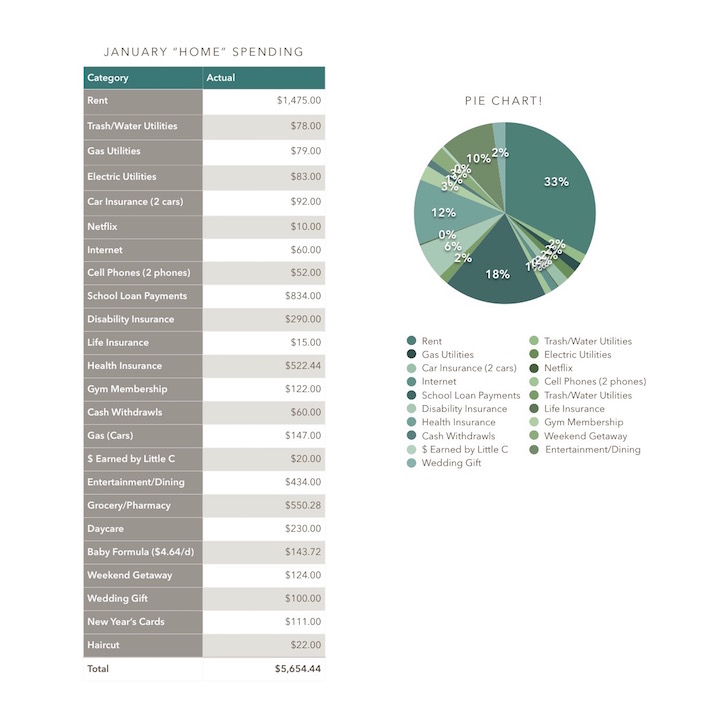

Without further ado, here is our home/family spending for January of 2018, in the form of a sophisticated screenshot from a Numbers document:

Voilà. In case you can’t see the image, that grand total is $5,654.44.

Multiply that by 12 and you’ll notice we would be living what is, frankly, a life of total luxury on $67,853.28 per year after taxes, in a high cost-of-living area with two kids.

It was really hard to find any info on the average annual spending of doctors and their families, so I don’t really know where we stand relative to our peers (although I suspect our spending is below average). The only comparable disclosure of spending I could find from a doctor was by Physician on Fire in 2015-2016. You can read that here.

If you know of any other resources on how doctors spend money (or if you are doctor and you’re willing to share info about your own spending habits), please get in touch! Thanks in advance!

2 Replies to “January Spending Report”

Hey doc, I accidentally stumbled on your blog from Women’s Orthodontics group. I can say you got a new fan! I graduated the end of 2012, also love traveling, domestic and internationally, also the outdoors! But for now, my burning question for you is which app/program you use for your expense sheet? I’d like to start it right, again, for 2019. Thanks for sharing!

Maggie thank you so much for the compliment! This expense sheet is just a Numbers document.:P It helps me to have to enter everything manually – makes me really own my spending. If you want to get a little more sophisticated than a spreadsheet like this, I’ve got friends who love Mint And Personal Capital. Both have free versions. 🙂 Happy New Year!!!