Ferry Rides, Fireplaces, and Other July Spending

A quick reminder: these spending reports are an effort to keep myself accountable to the idea that doctors do not have to spend a totally ridiculous amount of money to live well and love life. We’re trying to do these spending reports for every month of 2018.

As I have mentioned before, we do not do traditional budgeting. You absolutely should do traditional budgeting if that works for you as a way to control your spending. More on this topic here.

Notes About July

July knocked it out of the park as our most expensive month so far this year. I probably waited this long to post about it because I was hoping that total number would somehow become smaller.

For starters, our mortgage is significantly more expensive than our rent ever was, and our spending on daycare is going up too. We’re not excited about either of these increases, but they will ultimately help us meet other longer-term goals.

“Home Spending” was one of the non-recurring culprits. This giant number was due to a brand new couch and the fact that our very old and very broken and very not-up-code fireplace had to be ripped out and replaced by someone who knew how to manage gas lines (and wasp nests, as it turned out). Despite our pride in our DIY skills and our love of saving money, we were very happy to pay the pros for the new fireplace install.

As of July, it’s been two years since we switched to Google’s Project Fi, and we discovered that in that in those two years we saved over $5,000 on said cell phones (or over $208 per month). So that was cheering.

July included the tail end of our family vacation to the midwest and a week-long family vacation to Camano Island, Washington. Per our usual, these trips were partially sponsored by our travel hacking hobby, but they still resulted in more restaurant meals and gasoline use than other times.

The beautiful island home we stayed at for free on Camano Island is yet another great example of why you should always say “yes!” when friends invite you to visit them.

We have been training hard for the Imogene Pass Run this summer. The IPR is a scary enough race that it makes us want to spend all of our summer running up and down mountains, which turns out to be a healthy and cheap way to pass time. We are doing most of our workouts on the wilderness trails in our area, and have dropped our gym membership for the time being.

If you’re interested, check out our spending reports for January, February, March, April, May, and June. June’s report contains totals for the half-year mark as well.

Notes About The Numbers

-I have not included our charitable giving here, which can be a very sensitive subject for a lot of people (especially those who feel like they are drowning in debt). But unless you yourself are about to starve or freeze to death due to lack of basic resources, I recommend you find at least one charitable organization you are really excited about and send them monthly donations via auto-draft, even if it’s a small amount. Many charities desperately need people who can commit to monthly financial support.

-This list does not include our HSA, stock investments, or our real estate investments. I am planning to write more about how we approach our savings and investments at some point.

-This list does not include business loan payments, professional dues, licensing fees, malpractice insurance, or other expenses that are due exclusively to our business ownership and – unlike my student loans – would go away if I sold the business and switched careers.

-The student loan payment shown here is what’s on auto-draft. You can read here about how we are paying extra on our loans every month in an effort to be done with them this year. I include student loans in “home” spending even though they are related to my career because they don’t go away no matter what I do career-wise.

-We have health insurance and an HSA though my husband’s work as a teacher, both of which are deducted directly from his paycheck. It’s actually a pretty great deal, all things considered. We pay out of pocket for dental care and eye care services as needed.

-All “Entertainment/Dining” expenses are 100% optional expenses. For us, these tend to be things like going to the movies and eating at Chick-fil-A.

-I include life and disability insurance in this list even though they are sort of related to work, because they are what protect our current lifestyle. My disability insurance is expensive because it is important to us to be able to pay off all our debts and live well even if I am unable to work.

-“Groceries” includes food, household items, medications, and toiletries purchased at Sam’s Club or grocery stores or Walgreens.

-This list does not include at-home babysitters, who we very occasionally pay in cash to watch our kids. Any at-home babysitters we pay are non-essential, although very much appreciated. The daycare/childcare shown is what we pay for while we are both at work (which is very much essential as long as we both want to work) and is listed under “Daycare/Childcare”.

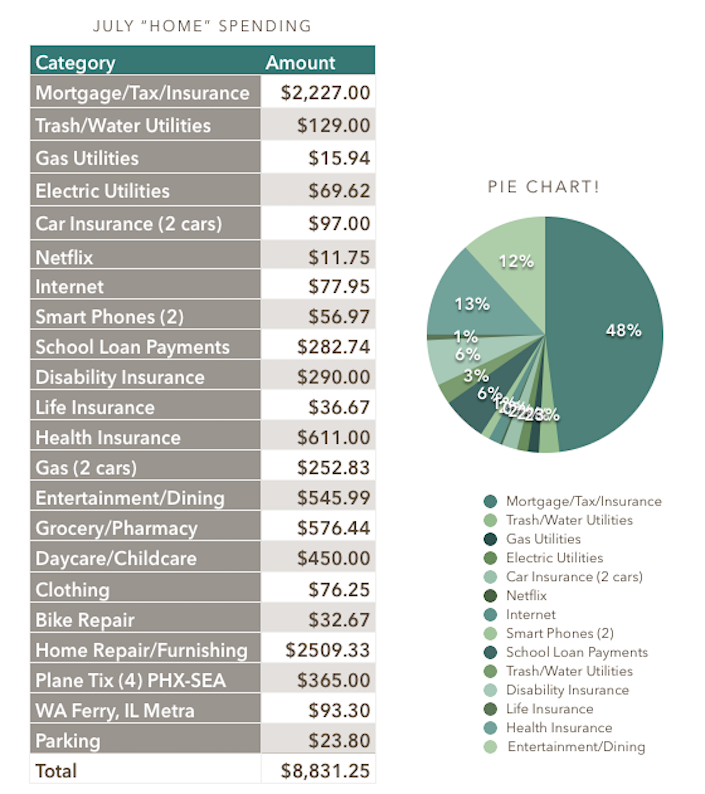

So here is our home/family spending for July of 2018, in the form of the sophisticated screenshot from a Numbers document that you’ve come to expect:

That total is $8,831.25, nearly $3k more than the current runner-up (March), which included a week in Maui.

Yikes. Let’s just move on to August. And never buy any new furniture ever again.